Aug 12

Flirting With a Bear

August 12, 2022

- Share:

-

-

-

-

With major stock indices in correction or bear market territory, many investors are watching their nest eggs shrink and wondering what to do. But market downturns are nothing new. It helps to learn from past bears and to take a long-term perspective.

For stock investors, the first five months of 2022 have not been pretty. As of May 31, the S&P 500 was down 14% from its early January high. The Dow Jones Industrial Average was off 10%, and the tech-heavy NASDAQ composite had fallen 24%. The NASDAQ is already in bear market territory -- defined as a drop of 20% or more from the most recent peak -- while the other two benchmarks are officially in correction territory -- a drop of 10% to 20% from the recent high.

The numbers are clearly troubling for anyone with a stock portfolio or a retirement savings account that holds stock investments. In fact, weathering a down market can be frustrating -- especially if you're using the same investing strategies that worked well when the market was on its way up. Surviving a bear market requires patience, a long-term perspective, and the use of different strategies to help minimize the impact of falling stock prices on your portfolio.

With major stock indices in correction or bear market territory, many investors are watching their nest eggs shrink and wondering what to do. But market downturns are nothing new. It helps to learn from past bears and to take a long-term perspective.

For stock investors, the first five months of 2022 have not been pretty. As of May 31, the S&P 500 was down 14% from its early January high. The Dow Jones Industrial Average was off 10%, and the tech-heavy NASDAQ composite had fallen 24%. The NASDAQ is already in bear market territory -- defined as a drop of 20% or more from the most recent peak -- while the other two benchmarks are officially in correction territory -- a drop of 10% to 20% from the recent high.

The numbers are clearly troubling for anyone with a stock portfolio or a retirement savings account that holds stock investments. In fact, weathering a down market can be frustrating -- especially if you're using the same investing strategies that worked well when the market was on its way up. Surviving a bear market requires patience, a long-term perspective, and the use of different strategies to help minimize the impact of falling stock prices on your portfolio.

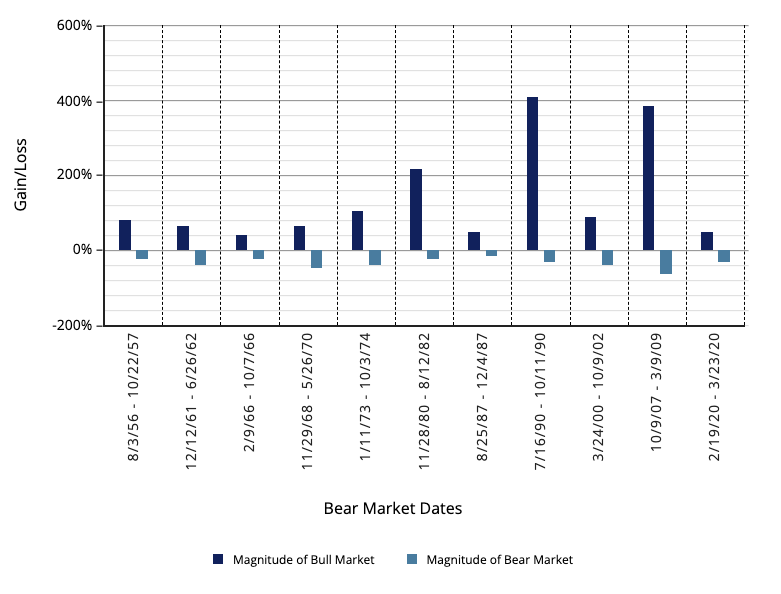

Better Than the Average Bear?1

Putting Market Returns in Perspective

Bear markets are nothing new. Between 1950 and 2021, there were 11 bear markets. The average bear market lasted about 14 months, with an average market decline of 34.2%. In contrast, the 10 completed bull markets during this time period lasted more than five years on average, with an average gain of 162.6%.2 The current routing follows a period of exceptionally strong returns. From 2017 through 2021, the S&P 500 recorded an average annual total return of 18.5%, and was up a whopping 28.7% in 2021. This compares with a long-term average return of around 10% since 1926. Clearly, part of what is happening today is a return to reality, albeit a grimmer reality characterized by inflation, rising rates, Covid, global supply chain disruptions, and a war in Eastern Europe. Where the market goes from here is anyone's guess. The question is: What can you do about it?Should You Sell?

Not surprisingly, the first reaction to a falling market is to bail out. But that kind of short-term thinking may not be in your best interest -- especially if you sell at a loss. Before selling, you should consider several factors. First, look at your time horizon; i.e., when will you need to use the invested funds? If you are investing for the long term -- for retirement, for instance -- then there's a strong likelihood that the market will rebound before you need to use the funds. Second, consider your alternatives. If you take your money out of equities, where will you invest it? Remember that in the long term, stocks have outperformed the other asset classes -- bonds and money market securities -- by a significant margin, although past performance is no guarantee of future returns. There's also tax to consider. If you liquidate stocks in a taxable portfolio, you will have to pay taxes on any capital gains.Maintain a Portfolio That's Right for You

If you haven't already done so, take a good look at your investments as a whole. What is your portfolio's asset allocation -- your mix of stocks, bonds, and cash equivalents? If you use your risk tolerance -- your emotional and practical ability to handle risk -- to guide the asset allocation process, you'll be better prepared to cope with market volatility. Reviewing your asset allocation can help you answer another question about your portfolio: Is it adequately diversified? In other words, have you spread your money among different investments to potentially help reduce risk? Different securities do better at different times. Therefore, holding a variety of investments creates the potential for those that perform well to compensate for those that do not over a period of time. Neither asset allocation nor diversification guarantees against investment loss. Finally, when assembling or maintaining a portfolio, consider tapping the expertise of a seasoned financial professional who has been through a number of market cycles. He or she can make suggestions regarding your portfolio mix, explain current market trends, and help you stay focused on your long-term financial goals. For more information about planning for your future, contact Popular's Retirement Center at educacionretiro@popular.com . If you have a 401(k) plan with Popular, remember that you can count on our group of experts at TeleBanco Popular® to guide you on issues related to your retirement plan. Call us at 787-724-3657 (press option 2 three times).Because of the possibility of human or mechanical error on the part of SS&C or its sources, neither SS&C nor its sources guarantee the accuracy, adequacy, completeness, or availability of the information and are not responsible for any errors or omissions or for the results obtained from using such information. SS&C will not be responsible or liable in any case for any indirect damage, special or consequential damages related to the use of the content by subscribers or other parties. © 2021 SS&C. Reproduction in whole or in part without prior permission is prohibited. All rights reserved. We are not responsible for errors or omissions. The information provided in this article has been provided for educational purposes and for your independent consideration. Any description included is for informational, educational and independent consideration purposes only; it is not to be considered, or viewed, as personalized investment advice or recommendation or as a suggested course of action to take (or refrain from taking) any particular action. By providing this information, we assume that you are able to evaluate this information and the general descriptions found here to exercise your independent judgment. Banco Popular de Puerto Rico, its subsidiaries, and/or affiliates, are not engaged in rendering legal, accounting or tax advisory services. If legal, accounting, or tax advice services are required, you should seek the services of a competent professional. Investment products are not FDIC insured, are not deposits or obligations of, nor are they guaranteed by Banco Popular, its subsidiaries or affiliates, and may lose value.

1 Source: ChartSource®, DST Retirement Solutions, LLC, an SS&C company. Stocks are represented by the daily closing price of the S&P 500 index, an unmanaged index that is generally considered representative of the U.S. stock market. The percentage increase in the final period represents the gain through December 31, 2021. It is not possible to invest directly in an index. Index performance does not reflect the effects of investing costs and taxes. Actual results would vary from benchmarks and would likely have been lower. Past performance is not a guarantee of future results. © 2022 SS&C. Reproduction in whole or in part prohibited, except by permission. All rights reserved. Not responsible for any errors or omissions. (CS000144) 2 Source: DST Retirement Solutions, LLC, an SS&C company. Based on the daily price close of the S&P 500. A bear market is defined as the S&P closing at least 20% below its previous high. Its duration is the period from the previous high to the lowest close reached after it has fallen 20% or more. A bull market is measured from the lowest close reached after the market has fallen 20% or more to the next high. Average gain does not include the current bull market gain.